Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

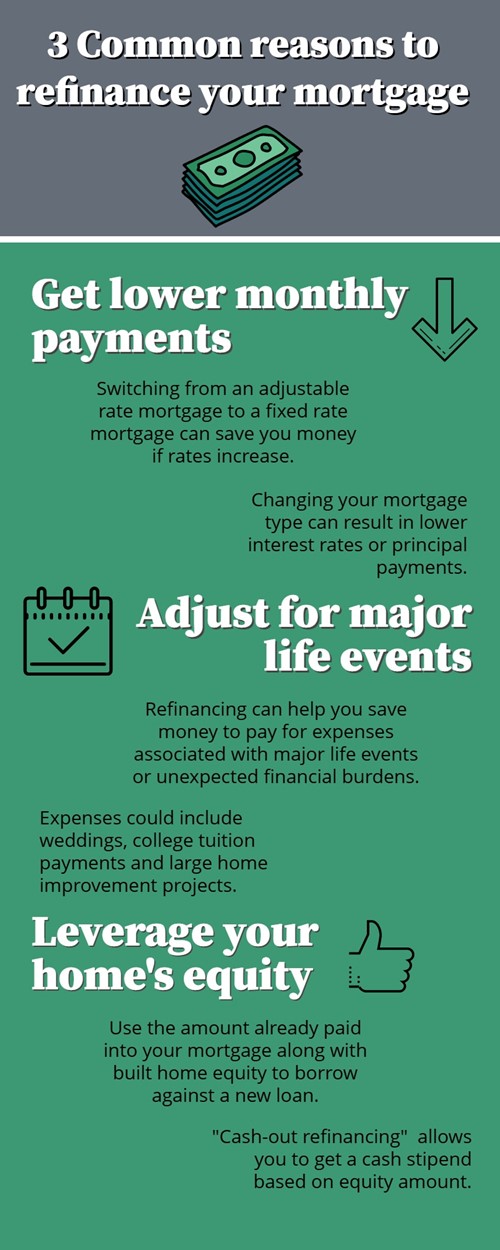

3 Common reasons to refinance your mortgage

Homeowners refinance their mortgages for an assortment of reasons. Some reasons center around strictly wanting to pay off their homes faster and at better interest rates, while others may fall along practical life events or emergencies. If you find yourself asking, “should I refinance my mortgage,” try checking off a few boxes to help come to a decision.

Here are a few reasons folks may refinance their fixed rate mortgage:

Lower monthly payment

One of the more upfront reasons to refinance a mortgage is to make your monthly mortgage payments more affordable. Some may even seek to reduce their monthly payments by switching their mortgage interest type from an adjustable rate mortgage to a fixed rate mortgage, especially if the interest rates start to creep higher than anticipated.

You’ll want to consider your current loan term against the refinanced loan term to determine if adding extra years or higher principal payments is worth refinancing before jumping into a new mortgage. Sometimes, the monthly savings fall below the lifetime savings of the loan and may not be worth the extra refinance fees.

However, if you find refinancing your mortgage puts you in a great financial place, and you don’t have any large changes in income or expenses coming your way, it may be a perfect time to refinance.

Life events

Sometimes, you may find you want to refinance your mortgage for life events such as weddings, school tuition, large home improvements or other personal expenses. If you find yourself in an emergency, you may also want to consider refinancing.

Regardless of your life event, consult your current mortgage lender to ensure you can refinance without breaking any terms or conditions set forward by the original agreement. If you can refinance, be sure to keep your finances as close to budget as possible, so you don’t end up with more debt or financial hardships than is necessary.

Home equity

After you’ve paid a decent amount into your mortgage loan, and have built some equity in your home, you can borrow more than your outstanding mortgage balance and receive the difference.

For example, if you’ve paid $50k into your current mortgage, with $150k outstanding, and want to refinance for a lower interest rate while getting more out of your home equity, applying for a new mortgage loan may be a great option. You could request $200k while using your home’s equity as a primary component for your new fixed rate loan.

Taking advantage of a “cash-out refinance” or “cash-out refi” gives you $50k to be placed back in your pocket for whatever projects or payments you want to use it for. Meanwhile, your new refinanced monthly payments may stay the same or lower, depending on the lender.

When refinancing your home, be sure to check in with your mortgage lenders. Some will offer you the options you’re searching for without having to switch to a new company that may not have your information on file or may request something deeper.

However, if you find a mortgage lender that checks all of your boxes, try contacting one of their loan officers to explore your options.

How to stay focused on home selling

As a home seller, it can be tough to balance both short- and long-term goals. However, taking key steps can help you pinpoint areas needing the most attention to help you streamline the process.

Establish a home selling timeline

A home selling timeline can help take the guesswork out of your home selling journey. Making a timeline, you can highlight your goals and when to execute them based on level of priority.

Consider making a timeline with a bit of flexibility to account for the potential of unexpected occurrences, whether that be a price change or a home improvement. Setting a timeline can help your home selling “train” stay on track.

Create home selling goals

By setting your home selling goals ahead of time, you give yourself the chance to exert your energy efficiently. They can also enable you to enjoy a sense of accomplishment as you finish a wide range of tasks when you sell your home.

Goals may include getting professional pictures taken or depersonalizing the property. You can set however many goals you see fit to best fit your needs as a home seller.

Work with a real estate agent

If you’re unsure about what to expect during the home selling journey, you may want to collaborate with a real estate agent. With their knowledge, they can help you identify areas needing improvement and attention and can help you accomplish steps towards your end goal of getting your home sold.

They can help promote your listing, point you in the direction of other real estate professionals if needed, and help you prepare to list competitively.

Using the aforementioned tips and tricks, you can remain on track throughout the home selling journey.

3 Things homeowners wish they had done differently before buying a home

Deciding to purchase your first home is a huge step, as it’s often a long term financial commitment. Studies have found, as much as 70 percent of homeowners have at least 1 regret regarding their property.

Understanding common homebuyer regrets can help guide you during the homebuying process towards a home you can be truly happy with for years to come.

Forgetting to research the neighborhood

It’s easy to become so focused on a home itself that you neglect to account for its surroundings. The neighborhood your home is located in can have a large effect on your daily life, so consider accounting for aspects of the neighborhood you and your household can enjoy.

If you have young kids, you may want to be located near parks and good school districts. Is the location of the home near grocery stores, your job, medical facilities? Acknowledging your lifestyle can help you pick a home in a neighborhood you’ll love.

Getting pressured into making a decision

Sometimes, a seller may portray their home as being highly sought after to encourage higher and more frequent offers. Similarly, you may find your household has time constraints and want to make a quick home purchase.

With all the pressure, it may be easy to settle for a home to meet a deadline or feeling like a property of interest will be unreachable if you don’t act fast. However, taking your time can help you and your real estate agent examine all details to figure out if this is a good long-term investment.

Forgetting you might someday have to sell the home

Sometimes, properties can be difficult to sell due to factors such as their location and surroundings. For instance, a remote home or one that is located too close to loud areas may not matter to you, but they may deter potential homebuyers.

This lesson also holds true for what you do with your home once it’s purchased. Making flashy renovations or design choices may not appeal to the average homebuyer and can make your home more difficult to sell.

Using the aforementioned tips, you and your real estate agent can do the research and take the time to figure out if the home you’re interested in is the most fitting choice.

Adjustable rate mortgages: pros & cons

If you’re shopping for a mortgage, you’ll need to choose between a fixed-rate mortgage (FRM) and an adjustable-rate mortgage. An adjustable rate mortgage (ARM) might seem like the best option because of low introductory rates and flexibility. However, there are some disadvantages to ARMs to consider carefully. Here are some of the main pros and cons of adjustable-rate mortgages:

ARM pros

- Low intro rates: An ARM usually offers a very low-interest rate for a fixed amount of time at the beginning of the loan. Depending on the terms of the loan, this means you’ll have the same low rate for the first several years before the payments increase. This is a major advantage for monthly budgeting: your payment will always be the same amount during that period.

- Flexibility: ARMs can be good choices for homebuyers who expect their lives to change within the next few years. For example, if you plan to change careers, start a family or sell your home for any other reason, you’re free to do so during your fixed-rate period.

ARM cons

- Payments will likely increase: Once your fixed-rate period is over, your interest rate will change–often for the worse. If interest rates in the market have risen since buying your home, you’ll have to start paying at the new rate at the end of your intro period. Not only will these payments be larger, but they won’t have any guarantee of remaining the same. This can make budgeting difficult.

- Prepayment penalty: A prepayment penalty is a fee that the lender can charge if you either refinance the loan or sell the home. Unfortunately, these penalties are commonly included in ARM terms. If you decide to move within the first five years of your mortgage, you could end up paying a steep penalty.

Mortgages are complicated, and the more you understand about your options, the more comfortable you’ll be in your financial decisions. When choosing between an FRM and an ARM, consider these pros and cons to choose the best fit for your situation.

4 Tips to get the best deal on your first home purchase

As a first-time homebuyer, you may find yourself asking, “what can I do to get a great deal on my first home?”

Purchasing a home is a financial decision that can potentially affect your finances for years to a whole

lifetime.

To make sure you get an affordable home matching your homebuying goals, it’s best to take a few key steps to give

yourself the best advantage during the home purchasing process.

Pay off small debts

A great way to prepare financially before applying for a mortgage loan is to pay off any small debts you have to

increase your credit score. Paying off debt at the current moment frees up some of your finances in the future,

giving you more funds to work with while lowering your debt-to-income ratio, which can earn you brownie points with

lenders.

A great end goal is to pay off your balance in full each month while avoiding interest and still earning rewards and

building credit.

Refrain from opening up new credit accounts

If you intend to apply for a mortgage loan in the near future, it’s best to avoid opening up new lines of credit

accounts that can temporarily lower your score. If you need to open a new credit line to boost your score, then do

so well in advance of applying for a mortgage.

Save for a home down payment

Saving money for a home down payment may seem taxing; however, it helps to be intentional with your savings.

Start by opening a dedicated bank account and direct-depositing a portion of your income into the account each week

or biweekly to continually grow your home purchasing funds.

To expedite your saving process, consider placing savings into a CD account or high-yield savings account. These give

the highest earnings from interest out of any other form of savings. Kindly note, these saving methods do make it

more difficult for you to pull money from the account to help users refrain from withdrawing money

unnecessarily.

Figure out how much house you can afford

Before purchasing a property, you’ll need to find out what is a reasonable amount to spend on a home. To accomplish

this, you’ll need to consider your monthly mortgage, recurring bills, taxes, insurance, and any other expenses

affecting your finances. Leave yourself room for savings, emergencies and wiggle room for fun expenses.

With the aforementioned tips, you can prepare for homeownership like a pro, and ease some tension of the homebuying

process.

How to prepare for day of closing

At the end of a long homebuying process, you’ll finally reach your goal: the day of closing. However, even though you’re at the finish line, closing on a new home is a process itself.

There are many steps to finalize your home purchase and just as many opportunities for delay. To make sure you’re prepared for closing day, here is a guide of what to have with you:

Photo ID

On closing day, you’ll need to confirm the identity of everybody named on the loan. If more than one person is listed, make sure they have their form of photo identification to show the title company.

Cash to close

Cash to close refers to the final closing costs you need to pay. Request a cashier’s check from your bank that covers final costs like down payment, prepaid interest, property taxes and insurance fees.

Closing disclosure

The closing disclosure is essential to finalizing your loan process. These documents include the final terms and details of your mortgage loan. Your lender can provide you with this information a few business days before closing.

Proof of insurance

Bring proof of your homeowners insurance policy at closing. Lenders require proof of insurance as a condition of loan approval. Have a copy of your policy declaration page from your insurance provider to show your mortgage lender.

Your real estate agent

Closing day is made up of several important legal transactions, and it’s important to have professional representation. Your real estate agent should be there to protect your interests and provide any guidance during the closing process.

Closing on a home is a major event. Not only is it the final step of your long buying process, it’s a process in itself. Remember this guide when preparing for closing day to ensure it goes smoothly and quickly.

Property tax deferment: The basics

In some states, qualified homeowners can use a property tax deferment to save on annual expenses. While deferring taxes usually refers to a period of delay in paying taxes on an item until a later date, property tax deferment comes with some additional important factors. Here is a quick guide about property tax deferrals:

How does it work?

Property tax deferment allows qualified homeowners to discontinue their real estate property taxes, as long as they remain qualified. While the taxes are deferred, there is a tax lien on the property. Interest will still accrue even if you’re not making payments, and unpaid taxes will appear with a “delinquent” status on public records.

Who qualifies?

Specific qualifications vary by state, but senior citizens and homeowners with disabilities may qualify for a property tax deferment. However, the general rule only applies to the property serving as your primary residence. Therefore, if you qualify for a deferral but move to another home, taxes on the old property will resume. Check with your local government to find out what opportunities you have to delay your tax payments and what your responsibilities are as a new homeowner.

What happens next?

Tax deferrals do not last forever. If the deferral ends due to a home sale or inheritance, the tax collection will resume and require payment of the entire deferred amount. This amount would include interest accrued during the deferral period.

While property tax deferment can be a huge benefit to homeowners, the taxes still need to be paid eventually. Therefore, when considering a new home, it’s crucial to investigate the tax situation to make the best financial choice.

Pros & cons of no-closing-cost refinancing

Refinancing your home can have a plethora of benefits. Among lowering your monthly payment, refinancing your home can also allow you to borrow against your home’s equity. However, refinancing in the beginning can have significant closing costs, such as application fees, loan origination fees, mortgage insurance and interest – especially when involving mortgage points.

Your new mortgage’s closing cost could have upfront fees of anywhere from 2% to 5%. However, there is another type of refinancing option available for homeowners who’d prefer to roll their closing costs into their monthly payments.

Here are the pros and cons of no-closing-cost refinances:

Pro: No closing costs

With no-closing-cost mortgage refinancing, you typically don’t have any upfront closing costs. In fact, your closing costs are rolled into your monthly mortgage payment, so you don’t have to worry about interfering with your current budget.

Con: Higher monthly payment

Because there are no upfront closing costs for a no-closing-cost refinance option, you may have higher monthly payments than if you’d chosen a cost-refinance method. However, higher monthly payments may not be the agreed term for rolling your fees into your new mortgage. Higher interest rates or a longer loan term are also viable options.

Pro: Immediate budget impact

If you’re taking out a no-closing-cost refinancing loan, you’re probably in the market for holding on to your budget at that time. This refinance option allows you to maintain your current budget and can give you the cash needed for other projects, responsibilities or emergencies.

Con: Monthly budget impact

If you are saving for something or budgeting for a big project, you could be set back a bit by the amount you’ll have to pay on your new monthly mortgage payment. Because the fees are rolled back into the loan itself, your monthly payments may be higher than originally anticipated, putting a hurdle in your savings plans.

Regardless of your reasoning for pursuing a no-cost-refinancing option, knowing both sides of the coin can help you make a more informed decision. Both types of refinancing are great options, and if you have questions about which to choose, try speaking with your agent or a finance professional employed with your current mortgage lender.

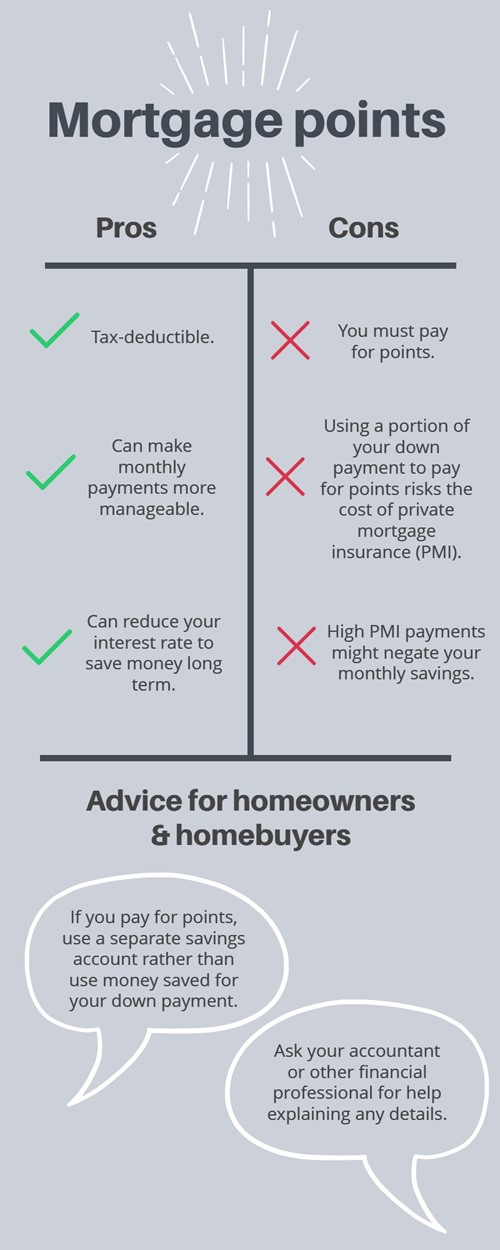

The pros and cons of mortgage points

When buying a home, many homebuyers tend to search for the best mortgage interest rates available. While some may find that perfect rate, others may opt to take advantage of lender-provided options, such as mortgage points.

Mortgage points are designed to help buyers bring down their interest rates by paying them ahead of time. Sometimes considered “discount points,” mortgage points allow you to pay a larger down payment up front to quell your interest rates throughout the life of your loan.

While that sounds like an excellent option for those searching to put a dent in their future monthly payments, there are a few items to consider.

Here are some pros and cons of mortgage points and tips on what to do for your situation:

Mortgage point pros

When delving into the world of mortgage discount points, the immediate hook is your monthly savings in the long term. Mortgage points are exceptional ways to bring your mortgage interest rate into a desirable range, creating more manageable payments on a monthly basis.

Another fantastic feature of mortgage points is they’re tax-deductible. According to the IRS, you can itemize your deductions on a Schedule A, or Form 1040, and only need to meet a few requirements, such as using the “cash method” for tax reporting. You’ll also need to have your primary residence as the loan’s security method.

Mortgage point cons

There are great advantages to discount points. However, there are a few cons that may surface with this kind of lender program. For example, if you plan to pay for mortgage points, try to secure a secondary savings account to make that payment instead of taking it from your down payment.

If you take the funds from your initial down payment, you could end up paying less than the 20% needed to avoid private mortgage insurance, or PMI. Since PMI can increase your monthly payments, you may end up paying more on your monthly mortgage than you’d save, or you could end up pushing out your break-even point, prolonging your larger payments.

Homeowner and homebuyer advice

There are ways to use mortgage points to your advantage. For starters, make sure you have an in-depth understanding of your current monthly finances, your projected finances and a financial roadmap for the next few years that you can follow easily.

Another fantastic idea is to get in touch with your loan officer or lender. Have them explain your options, what the estimates are for the next few years (or further) and any tips they may have for you. If you find yourself in the beginning stages of your home search, ask your real estate agent for any connections or recommendations to a lender or loan officer.

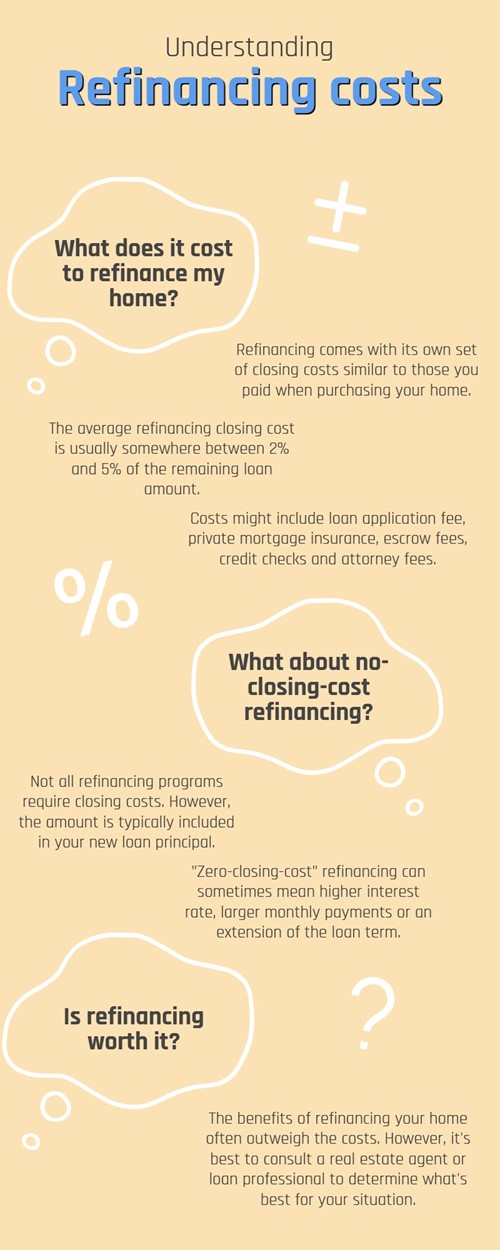

Home refinance: Costs to consider

Refinancing your home can have major benefits: a lower monthly payment, cash use of home equity for a variety of purposes, generate more appetizing mortgage terms, etc. However, there are a few things to remember when entering into a mortgage refinance, like refinance cost.

Here are a couple of cost options to remember when you’re ready to refinance your home:

Traditional closing costs

The biggest group of refinancing costs that you should be aware of is the closing costs. While you may not have to pay the same closing costs you did when you first purchased the house, there’s a good chance you’ll need to pay at least 2% of the remaining mortgage loan, but typically no more than 5%.

Average closing costs may include your loan application fee, private mortgage insurance, escrow fees, credit checks, attorney fees and any other property-related payments. However, these fees are based on the individual loan provider

No-closing-cost refinancing

Some refinance programs don’t require you to pay closing costs. No-closing-cost refinance options are often considered if the closing costs on your new loan don’t quite fit into the budget. The costs are typically added in with your new loan principal and may come up as higher interest rates, larger monthly payments or an extension of the loan term.

Refinance closing costs are typically part of the refinancing game, which may cause some homeowners to turn away from refinancing. However, the benefits of refinancing may outweigh the costs, and with a plethora of options available for a variety of financial situations, there’s a good chance you’ll find the right mortgage refinancing program for your circumstance.

If you need an extra bout of insight but don’t know where to start, try your real estate agent and the network of loan and finance professionals they may have at their disposal.